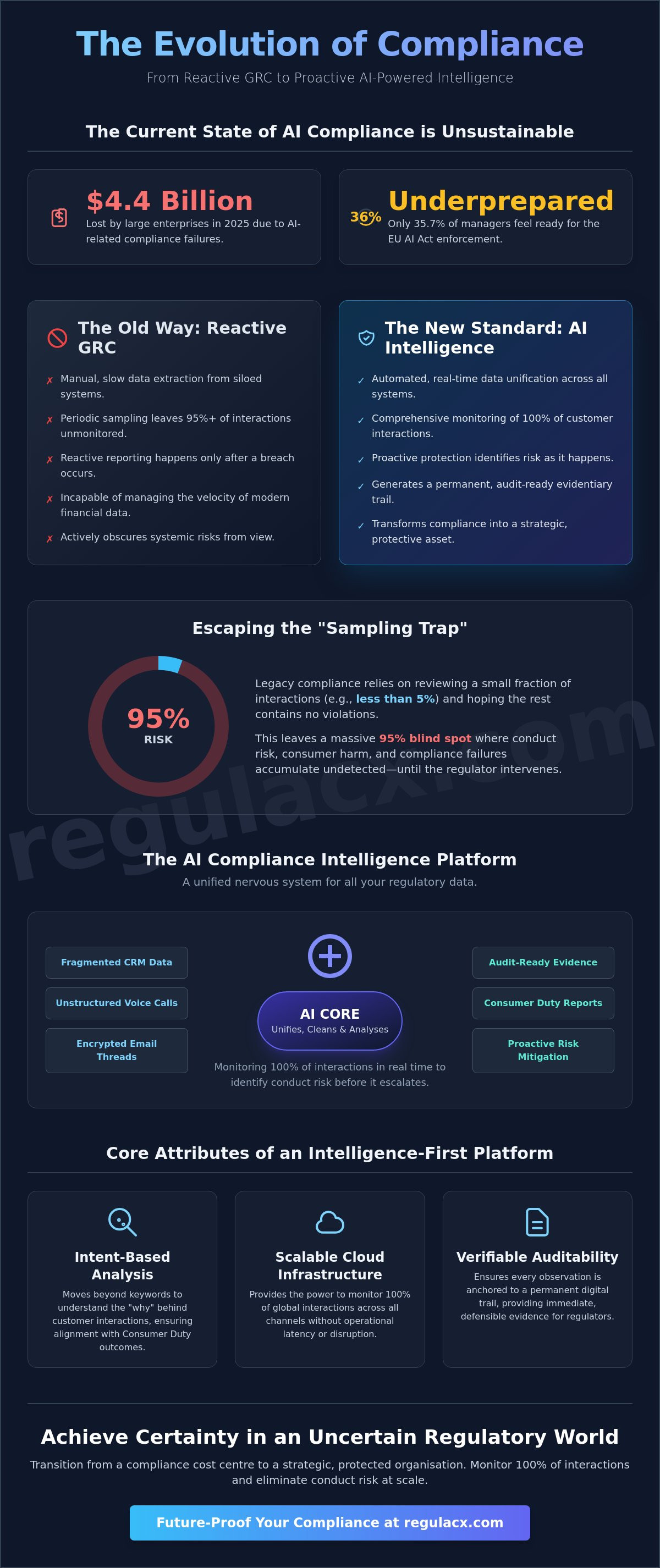

In 2025, large enterprises absorbed $4.4 billion in financial losses due to AI-related compliance failures, yet only 35.7% of managers feel prepared for the stringent enforcement of the EU AI Act arriving this August. You likely recognise that manual data extraction from legacy systems cannot keep pace with the FCA's demand for granular, real-time oversight. Relying on periodic consultancy or sampling a fraction of customer interactions leaves dangerous gaps in your conduct risk profile; it's a vulnerability that high-stakes environments can no longer afford. This guide demonstrates how a sophisticated AI compliance intelligence platform unifies disparate data streams to automate Consumer Duty evidence and eliminate conduct risk at scale.

The transition from voluntary frameworks to enforceable rules demands a fundamental shift in strategy. It requires moving beyond external horizon scanning toward internal data unification. We will examine the technical architecture required to generate audit-ready reports without manual intervention, ensuring your organisation remains resilient against regulatory scrutiny whilst significantly reducing the cost of compliance. By monitoring 100% of customer interactions and customer interaction risk, you establish a new standard for transparency and accountability that satisfies the most rigorous regulatory expectations.

Key Takeaways

- Understand why an AI compliance intelligence platform is the essential successor to legacy GRC systems, serving as a unified central nervous system for complex regulatory data.

- Discover how to integrate fragmented CRM data with unstructured interaction records to achieve comprehensive, real-time oversight across all communication channels.

- Abandon the inherent risks of manual sampling by implementing automated monitoring that covers 100% of customer interactions without increasing operational headcount.

- Secure a permanent, audit-ready evidentiary trail to satisfy the FCA’s rigorous shift toward outcomes-based regulation and Consumer Duty mandates.

- Transition from reactive reporting to proactive protection by leveraging cross-system data unification to identify and mitigate conduct risk before it escalates.

Beyond Traditional GRC: The Rise of the AI Compliance Intelligence Platform

Legacy oversight is no longer a viable defence. For decades, firms relied on traditional Governance, Risk, and Compliance (GRC) frameworks to manage their obligations. These systems served as external repositories for policy documents and risk registers; they were passive observers rather than active participants. In 2026, the regulatory climate has shifted from voluntary principles to enforceable, high-stakes mandates. An AI compliance intelligence platform represents the necessary evolution of this architecture. It doesn't just record rules; it understands the data flowing through your systems in real time.

The distinction is critical. Traditional GRC tools are reactive, focusing on reporting after a breach has occurred. Conversely, intelligence-led platforms act as a vigilant guardian, identifying conduct risk at the moment of interaction. As enforcement of the EU AI Act reaches its pivotal August 2026 deadline, the demand for a technical insider approach to data has become absolute. Firms can't afford to remain blind to the sentiment and intent buried within millions of customer conversations. A modern platform provides the intellectual rigour required to bridge the gap between high-level oversight and granular evidence.

The Limitations of Legacy Compliance Software

Static spreadsheets and manual trackers are fundamentally incapable of managing the velocity of modern financial data. They create siloes where compliance teams operate in isolation from the actual customer interaction data. This architectural flaw leads to the "Sampling Trap," where firms review a mere fraction of interactions and hope the remaining 95% contains no violations. The cost of this hope is staggering. With large enterprises having faced $4.4 billion in AI-related losses in 2025, the investment in modern intelligence is a matter of institutional survival. Siloed tools don't just fail to protect; they actively obscure the systemic risks that lead to FCA intervention.

Core Attributes of an Intelligence-First Platform

A true AI compliance intelligence platform must possess architectural depth that exceeds simple keyword matching. It requires precision-led data ingestion that parses complex human behaviour, identifying subtle indicators of vulnerability or dissatisfaction that manual reviews miss. Every observation must be anchored to a digital paper trail to ensure permanence. Key attributes include:

- Intent-Based Analysis: Moving beyond "what" was said to "why" it was said, ensuring every interaction aligns with Consumer Duty outcomes.

- Scalable Cloud Infrastructure: Providing the computational power to monitor 100% of global interactions without latency.

- Verifiable Auditability: Ensuring that when regulators demand proof, the evidence is immediate, defensible, and securely logged.

This intelligence-first approach ensures that compliance is a continuous, automated process rather than a periodic burden. It transforms oversight from a cost centre into a strategic asset that provides absolute certainty in an increasingly complex regulatory environment.

Architecting Oversight: How Cross-System Data Unification Powers Real-Time Monitoring

The primary barrier to effective oversight isn't a lack of data; it's the fragmentation of that data across incompatible architectures. Financial institutions operate within a chaotic ecosystem of structured CRM entries, unstructured voice recordings, and encrypted email threads. Without a centralised mechanism to harmonise these streams, conduct risk remains hidden in the gaps between systems. An AI compliance intelligence platform serves as the central nervous system for this regulatory data, ingestng disparate inputs to create a singular, verifiable record of customer interaction. This process requires more than mere storage. It demands the rigorous cleaning and categorisation of data to ensure that the resulting analysis is defensible during an audit.

Immediacy is the new benchmark for regulatory excellence. Batch processing, whilst once the industry standard, is now a liability. Waiting for weekly or monthly reports to identify a breach means the damage is already done and the evidence is already stale. Real-time monitoring allows for the instant detection of anomalies, moving the compliance function from a post-mortem exercise to an active intervention. This level of precision aligns with the NIST AI Risk Management Framework, which emphasises the need for trustworthy and resilient AI systems in critical infrastructure. Adopting a strategy of cross-system compliance data unification ensures that your oversight is as dynamic as the markets you operate in.

Breaking Down Data Silos in Financial Services

Legacy banking systems were never designed for the era of AI-driven scrutiny. These siloes prevent a holistic view of the customer journey, making it impossible to track outcomes across multiple touchpoints. Integration requires a sophisticated layer of Natural Language Processing (NLP) to interpret the nuance of human speech and text. By deploying modern APIs that bridge the gap between legacy cores and intelligence layers, firms can maintain data integrity whilst extracting actionable insights. This technical integration is the only way to satisfy the ISO/IEC 42001:2023 standard for AI management systems, ensuring every data point is accounted for and every interaction is transparent.

The Mechanism of Real-Time Risk Detection

Detection at scale requires the platform to distinguish between routine queries and high-risk indicators, such as "vulnerable customer" signals, amongst millions of data points. Automated alerting systems bypass the delays of manual review, notifying compliance officers the moment an interaction deviates from established safety parameters. This shift from sampling to total coverage is what defines modern conduct risk management.

Data Unification in the context of conduct risk is the architectural process of aggregating and normalising disparate structured and unstructured data streams into a single, verifiable source of truth for automated evidence extraction.

By establishing this foundation, firms move beyond simple monitoring. They create a proactive shield that identifies systemic issues before they manifest as regulatory interventions. The result is a streamlined, efficient oversight model that values technical proof over general claims of compliance.

Detecting Conduct Risk: Why Automated Intelligence Surpasses Manual Sampling

Manual sampling is an institutional gamble. Reviewing a mere 5% of customer interactions leaves 95% of your firm's conduct risk entirely unmanaged; it's a structural weakness that regulators no longer tolerate. An AI compliance intelligence platform replaces this probabilistic approach with absolute coverage. By analysing every interaction, the platform identifies systemic failures that human reviewers, constrained by time and cognitive bias, inevitably miss. This transition from "checking boxes" to "analysing outcomes" is the defining shift of the 2026 regulatory landscape.

Machine learning models are now sophisticated enough to detect "sludge practices", which are subtle, intentional friction points designed to discourage customers from exercising their rights or obtaining better outcomes. These patterns are often invisible in isolation but become glaringly obvious when viewed across a firm's entire dataset. This level of scrutiny is increasingly necessary as federal AI compliance mandates highlight the complexities of maintaining rigorous oversight in automated environments. Firms must move beyond reporting what happened to understanding why it happened at scale.

Quantifying the Accuracy of AI vs. Human Review

Human review is inherently subjective. Different compliance officers often interpret the same interaction through varying lenses of risk, leading to inconsistent reporting. Standardised AI models eliminate this inconsistency, applying a uniform set of evidentiary rules to every transcript and data point. The speed advantage is equally transformative. Whilst a manual audit of ten thousand calls might take weeks, an AI compliance intelligence platform can process a year's worth of data in minutes. Detecting a single systemic issue, such as a misaligned incentive structure, early in the lifecycle saves millions in potential remediation and prevents the reputational damage of a public FCA intervention.

Addressing the "Black Box" Objection

Transparency is the cornerstone of defensible compliance. Modern platforms have moved beyond opaque logic to provide full explainability for every risk flag. When a system identifies a potential conduct breach, it provides the specific technical evidence and linguistic markers that triggered the alert. This empowers compliance officers to act as the final authority, using AI as a precision tool rather than a replacement. Human-in-the-loop architecture ensures that technical intelligence is always tempered by professional judgement, creating a robust, audit-ready oversight framework.

Total automated monitoring is the only defensive posture that provides the evidentiary weight required to satisfy modern outcomes-based regulatory standards.

Evidencing Consumer Duty: Establishing a Permanent, Audit-Ready Trail

The FCA's shift to outcomes-based regulation marks the end of plausible deniability. Regulators no longer accept high-level policy statements as proof of compliance; they demand empirical evidence that customers are receiving fair treatment. An AI compliance intelligence platform provides this proof by generating a continuous, immutable record of every interaction and its subsequent outcome. It's no longer sufficient to state that your processes align with the Duty. You must demonstrate it through defensible data. This requires a transition from static documentation to a dynamic evidentiary trail that survives the most rigorous supervisory scrutiny.

Maintaining a permanent state of audit-readiness is the only viable strategy for high-stakes financial environments. When the FCA conducts an unexpected visit, the burden of proof rests entirely on the firm. A platform that unifies interaction data ensures that the evidence is already compiled, verified, and ready for inspection. This eliminates the panicked, manual data extraction that typically precedes a regulatory deadline. By establishing a transparent architecture, you signal to regulators that your oversight is both vigilant and technically sophisticated.

Outcome-Specific Evidence Automation

- Products and Services: The platform monitors interactions to verify that offerings remain fit for purpose for the target market. It flags instances where products are sold to unsuitable cohorts or where marketing fails to meet complexity standards.

- Price and Value: AI models analyse fee structures and service delivery to justify value assessments across the entire portfolio. This ensures that the price paid is consistently proportionate to the benefit received.

- Consumer Understanding and Support: By tracking the effectiveness of customer communications in real-time, the platform identifies where explanations fail or where support is insufficient. It provides the technical proof that customers can make informed decisions.

The Anatomy of an Audit-Ready Report

Generating board-ready reports should not be a manual burden. In a high-responsibility environment, the delay caused by manual data entry is a risk in itself. Automated reporting systems extract the necessary metrics directly from the unified data layer, ensuring that the information presented to the board is accurate, current, and free from human error. Every report must contain specific technical components to be considered defensible:

- Data Source Integrity: A clear link to the original interaction, whether voice, email, or chat.

- AI Observation: The specific linguistic markers or behavioural patterns identified by the model.

- Risk Rating and Remediation: A calculated severity score and a record of the corrective action taken.

- Timestamped Verification: Proof of continuous compliance over time rather than a snapshot taken just before a filing deadline.

To secure your organisation's regulatory standing and eliminate reporting gaps, implement Consumer Duty monitoring and evidence automation today. This transition ensures that your compliance function remains a proactive shield rather than a reactive cost centre.

The RegulaCX Advantage: Future-Proofing Financial Oversight in 2026

RegulaCX represents the logical apex of the 2026 regulatory shift. It integrates the architectural requirements of an AI compliance intelligence platform into a single, defensible interface designed for high-stakes financial environments. By automating the oversight function, firms eliminate the reliance on external consultancies that provide only snapshot views of risk. This transition from "rented" compliance to "owned" intelligence ensures that protection is continuous, not episodic. Permanent software monitoring provides a level of depth that manual audits cannot replicate, identifying systemic issues before they manifest as regulatory interventions.

Transitioning from manual chaos to automated certainty requires a structured approach to data normalisation. The path to implementation begins with the unification of existing data streams, normalising the flow of information without disrupting core banking operations. This moves the organisation away from the inefficiency of fragmented reporting toward a streamlined, evidence-led model. By establishing this technical foundation, your firm secures a permanent state of audit-readiness that satisfies the most rigorous supervisory queries from the FCA and other global regulators.

Seamless Integration, Absolute Certainty

Our platform unifies existing CRM entries, voice recordings, and email threads without requiring a total system overhaul. This preserves institutional stability whilst injecting modern, precision-led intelligence into the compliance function. The RegulaCX "Vigilant Guardian" philosophy ensures 24/7 monitoring of interactions and complaints, providing a level of oversight that human teams cannot achieve alone. Every data point is categorised, every risk is flagged, and every outcome is recorded in a verifiable evidentiary trail. Explore the capabilities of our AI-Powered Compliance Intelligence Platform to understand how we bridge the gap between legacy data and modern regulatory demands.

Securing the Future of Your Organisation

Integrity is now a primary competitive advantage. Firms that can prove their compliance to the regulator with immediate, defensible data operate with a level of operational freedom that their peers cannot match. Moving beyond "safe" to a "biologically optimal" compliance structure means your oversight is built into the very fabric of your operations. It scales as you scale. Protection is no longer a bottleneck; it's a foundation for growth. When your organisation can demonstrate 100% coverage of customer interactions, you establish a new standard for transparency and accountability that regulators respect.

The era of manual sampling and reporting gaps has ended. Secure your standing in the 2026 regulatory landscape by adopting a solution that values technical proof over general promises. Request a technical briefing on our Consumer Duty automation to begin your transition toward absolute oversight and automated certainty.

Securing Regulatory Leadership Through Automated Oversight

The 2026 regulatory landscape has no room for the structural vulnerabilities of manual sampling or reactive reporting. Transitioning to an AI compliance intelligence platform is the only way to ensure your organisation remains resilient against the FCA's outcomes-based scrutiny. Precision is no longer optional. By unifying disparate data streams and automating Consumer Duty evidence tracking, you replace operational chaos with technical certainty. Real-time conduct risk alerts and audit-ready reporting with zero manual effort allow your team to focus on strategic growth rather than evidentiary extraction. This architectural shift ensures that every interaction is monitored and every outcome is verified. It creates a permanent state of audit-readiness that satisfies the most rigorous supervisory queries.

Request an Audit-Readiness Assessment with RegulaCX to establish a new standard for transparency within your institution. You've the opportunity to transform compliance from a reactive burden into a proactive shield that protects your firm's integrity and its future.

Frequently Asked Questions

What is an AI compliance intelligence platform?

An AI compliance intelligence platform is a technical architecture designed to unify fragmented customer data and automate the detection of regulatory breaches. Unlike standalone tools, it integrates structured and unstructured data from CRM and voice systems to provide a singular source of truth. It acts as a vigilant guardian, scanning 100% of interactions to ensure every customer touchpoint aligns with internal policies and external legal obligations.

How does an AI compliance platform differ from traditional GRC software?

Traditional GRC software functions as a passive repository for policies, whereas an intelligence-led platform provides active, real-time oversight. Legacy systems rely on manual input and periodic sampling, which creates dangerous visibility gaps. A modern platform replaces these static trackers with automated workflows that identify risks as they occur. This shift from reactive reporting to proactive protection is essential for maintaining institutional integrity in complex financial environments.

Can AI really automate the evidence collection for the FCA Consumer Duty?

Yes, the platform automates evidence collection by mapping every interaction to the four Consumer Duty outcomes. It extracts specific linguistic markers and behavioural patterns to prove that products are suitable and communications are understood. This creates a continuous, timestamped log of compliance that requires zero manual intervention. By establishing this evidentiary trail, firms can demonstrate positive customer outcomes with absolute technical certainty during any regulatory inspection.

Is AI-generated compliance evidence acceptable to the FCA?

The FCA accepts AI-generated evidence provided the firm can demonstrate the logic behind the observations and maintain a transparent audit trail. Regulators prioritise the quality and accuracy of outcomes over the method of collection. An AI compliance intelligence platform ensures every risk flag is backed by specific data points, making the evidence defensible. This level of granular proof often exceeds the reliability of manual sampling methods traditionally used by compliance teams.

How long does it take to integrate an AI compliance platform with legacy systems?

Integration timelines vary based on the complexity of your legacy architecture, but modern API-led approaches significantly accelerate the process. Most firms can establish a unified data layer and begin monitoring interactions within a matter of weeks rather than months. Because the platform sits atop existing systems, it doesn't require a total infrastructure overhaul. This allows for a streamlined transition from manual data silos to a centralised, automated oversight model.

What is conduct risk detection in the context of AI?

Conduct risk detection involves the automated identification of patterns that suggest unfair customer treatment or systemic process failures. In an AI context, this means using machine learning to parse sentiment and intent amongst millions of data points. The platform flags subtle indicators of customer vulnerability or "sludge practices" that human reviewers might overlook. This ensures that potential breaches are identified and remediated before they escalate into significant regulatory liabilities.

Does an AI compliance platform replace the need for a compliance team?

No, the platform does not replace your compliance team; it empowers them to operate with greater precision and speed. By handling the high-density stream of data monitoring and evidence collection, the software frees professionals to focus on high-stakes decision-making and remediation strategy. It removes the burden of manual data entry and interaction sampling. This architectural support allows your experts to act as the final authority in a more efficient, tech-enabled environment.

How does the platform handle sensitive customer data whilst maintaining privacy?

Data privacy is maintained through rigorous encryption protocols and the automated redaction of Personally Identifiable Information (PII) during the analysis phase. The platform is designed to process interaction intent whilst ensuring that sensitive customer details remain protected according to global standards. Access controls and audit logs ensure that only authorised personnel can view the underlying data. This approach balances the need for total oversight with the absolute requirement for data integrity and privacy.