The financial penalty for regulatory failure in 2026 is no longer a mere cost of business; with non-compliance expenses now nearly triple the cost of proactive adherence, the margin for error has vanished. You're likely managing the daily friction of siloed data across legacy systems whilst facing the relentless manual effort required to unify conduct risk reports. The impending March 2026 implementation of the Homebuyers Privacy Protection Act, alongside shifting TILA thresholds, only heightens the urgency for absolute audit-readiness and technical precision.

This strategic guide reveals how sophisticated complaint monitoring compliance software enables your organisation to transition from reactive dispute resolution to a posture of proactive, automated conduct risk monitoring. We'll explore the architectural frameworks required for real-time visibility into customer interaction risks and the specific mechanisms for generating automated, audit-ready compliance evidence that satisfies the most rigorous regulatory scrutiny. By the end of this briefing, you'll understand how to integrate cross-system data to eliminate manual reporting burdens and establish a definitive evidentiary trail.

Key Takeaways

- Shift from reactive resolution to proactive detection; it's vital to identify why traditional ticketing systems fail to meet 2026 conduct risk standards.

- Utilise AI-driven architectures to unify disparate data streams and eliminate the manual burden of conduct risk reporting through automated data integration.

- Assess complaint monitoring compliance software based on its capacity to maintain data integrity whilst interpreting complex financial nomenclature.

- Secure an audit-ready posture through automated evidence tracking that's designed specifically for high-stakes financial environments and Consumer Duty requirements.

Beyond Resolution: The Regulatory Mandate for Complaint Monitoring

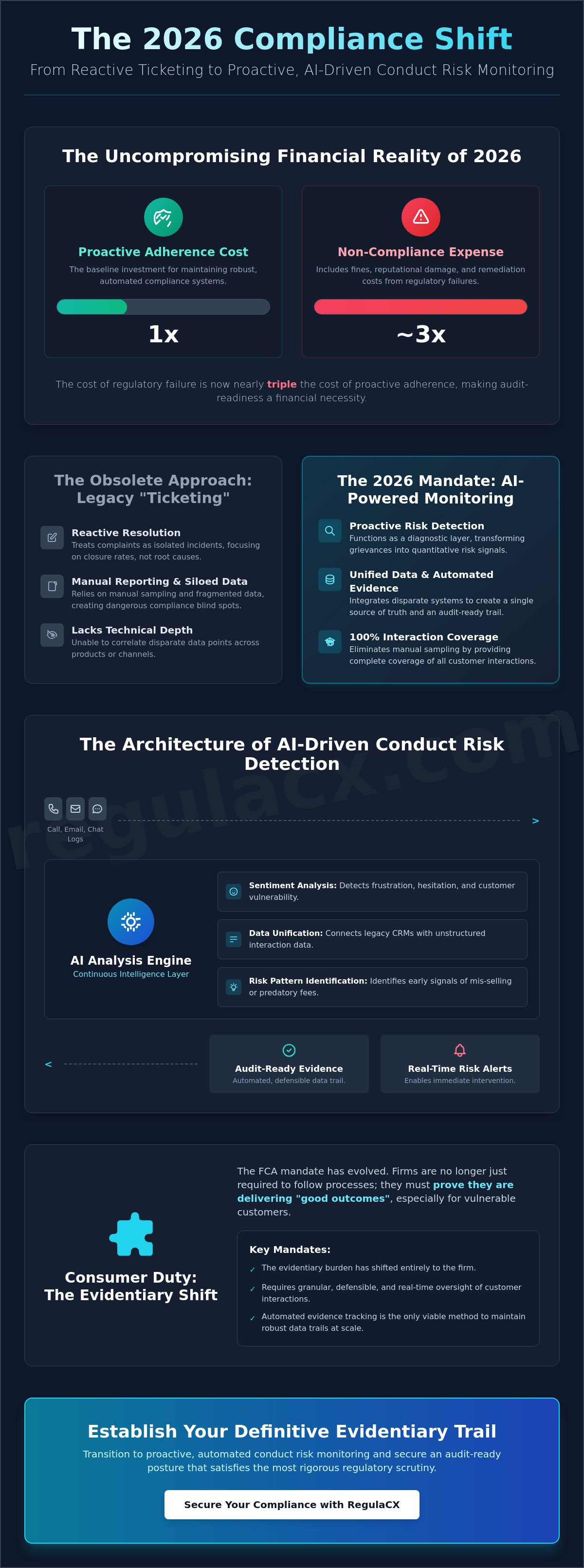

Resolution speed is an administrative metric. It is not a compliance outcome. For years, financial institutions utilised legacy complaint management systems to track ticket volumes and closure rates. This workflow-centric approach is now fundamentally obsolete. In the 2026 regulatory environment, complaint monitoring has transitioned from a back-office function to a core component of conduct risk architecture. It is the systematic extraction of intelligence from customer dissatisfaction to identify structural failures before they escalate into systemic crises.

Traditional "ticketing" systems fail because they treat complaints as isolated incidents. They lack the technical depth to correlate disparate data points across multiple product lines or communication channels. Modern complaint monitoring compliance software addresses this gap. It functions as a diagnostic layer. It unifies fragmented data. It transforms qualitative grievances into quantitative risk signals. By treating complaints as an early warning system, firms can detect emerging conduct risks, such as mis-selling or predatory fee structures, in real-time.

Consumer Duty and the Evolution of Oversight

The Financial Conduct Authority (FCA) has moved the goalposts. Under the Consumer Duty, the evidentiary burden has shifted. Firms are no longer just required to follow processes; they must prove they are delivering "good outcomes." This mandate necessitates real-time oversight of customer interactions. Oversight must be granular. It must be defensible. Firms must identify patterns of behaviour that suggest harm, particularly amongst vulnerable customers. Automated evidence tracking is the only viable method for maintaining the robust data trails required to satisfy these heightened regulatory expectations.

The Cost of Regulatory Non-Compliance

The financial reality of 2026 is uncompromising. Research indicates the cost of non-compliance is nearly triple the cost of maintaining proactive oversight. Inadequate conduct risk monitoring creates dangerous blind spots. These gaps allow systemic issues to fester, leading to catastrophic reputational damage and multi-million pound penalties. Manual sampling is no longer a defensible strategy. It is statistically insufficient for large-scale institutions. Complaint monitoring compliance software eliminates these vulnerabilities by providing 100% coverage of customer interactions, ensuring that no risk signal is ignored or lost in a siloed database. Precision is the only protection against regulatory scrutiny.

The Architecture of AI-Driven Conduct Risk Detection

The architecture of modern complaint monitoring compliance software is defined by its ability to synthesise raw data into defensible evidence. Legacy frameworks rely on manual oversight. They are inherently prone to fragmentation. AI-driven platforms instead establish a continuous intelligence layer that operates across every customer touchpoint. This isn't just about efficiency. It's about establishing a single source of truth that satisfies the regulatory mandate for complaint monitoring by ensuring no interaction remains unexamined.

Real-time interaction monitoring is the first line of defence. By ingesting call recordings, emails, and chat logs simultaneously, the system applies sophisticated sentiment analysis to detect more than just keywords. It identifies frustration, hesitation, and vulnerability. These are the precursors to conduct risk. When these signals are detected, the software flags them for immediate intervention. This proactive stance transforms the compliance function from a post-mortem auditor into a vigilant guardian. Data integrity is absolute. Precision is the priority.

Unifying Disparate Data Sources

Connecting legacy CRMs with unstructured call data is a significant technical hurdle. Most organisations struggle with data silos that obscure systemic failures. RegulaCX bridges this gap by acting as a cross-system intelligence layer. It unifies front-office interactions with back-office compliance requirements. By centralising these disparate streams in a cloud-based environment, firms gain absolute visibility. You can explore how cross-system compliance data unification eliminates these blind spots and creates a cohesive evidentiary record.

AI and Machine Learning in Risk Identification

The efficacy of complaint monitoring compliance software depends on the precision of its algorithms. Generic models fail in the high-stakes financial sector. Specialised machine learning models are required to detect specific patterns of behaviour, such as pressure selling or inadequate disclosure. These refined models significantly reduce "false positives," allowing compliance teams to focus on genuine threats. The result is a high-velocity risk detection engine. It moves faster than any manual review process could ever achieve. Regulatory certainty is assured through technical rigour.

Comparing Legacy GRC Systems with AI Compliance Intelligence

Legacy GRC systems function as archives. They record what has already transpired, offering a static view of historical failures. Whilst these systems of record were sufficient for the regulatory environment of the previous decade, they're fundamentally incapable of meeting 2026 standards. Modern complaint monitoring compliance software represents a paradigm shift from a system of record to a system of intelligence. It doesn't just store data; it interrogates it in real-time to identify patterns of conduct risk before they manifest as regulatory breaches.

The technical disparity between these two approaches is most visible in the speed of reporting. Manual evidence generation is a retrospective project that often takes weeks to complete. In contrast, an AI-powered intelligence platform provides instantaneous, defensible data. This speed is a strategic necessity. When regulators demand evidence of Consumer Duty compliance, the ability to produce automated, audit-ready reports within minutes provides a level of certainty that manual processes simply can't match. Precision is automated, not estimated.

The Manual Reporting Trap

Spreadsheets are the enemy of precision. Many organisations remain caught in a cycle of manual data collation, where compliance officers spend over 60% of their time reconciling disparate systems rather than analysing risk. This human-centric approach is fraught with risk. It's prone to error. It creates lag. More importantly, manual systems struggle to adapt to the velocity of regulatory change. When thresholds for credit transactions or mortgage-related inquiry rules shift, manual frameworks require extensive, time-consuming reconfiguration. This creates a window of vulnerability that regulators won't ignore.

Defining Compliance Intelligence

A true compliance intelligence platform is a proactive oversight tool. It establishes a permanent state of audit-readiness. Unlike legacy systems that require "clean-up" phases before an audit, modern software maintains data integrity continuously. This architecture offers several distinct advantages:

- Scalability: AI monitors 100% of customer interactions, whereas human-centric teams are limited to sampling less than 5% of data.

- Real-Time Alerts: Compliance officers receive notifications of interaction risks whilst they're still manageable, preventing escalation.

- Total Cost of Ownership (TCO): Whilst the initial investment in AI appears higher, the reduction in manual labour and the avoidance of non-compliance penalties results in a significantly lower TCO over time.

Key Criteria for Selecting Compliance-First Software

Selecting complaint monitoring compliance software requires a shift from operational convenience to regulatory rigour. You must evaluate a platform based on its native understanding of financial logic. A generic tool won't distinguish between a standard enquiry and a high-risk event under the July 2026 Regulation B amendments. It needs to recognise thresholds like the $73,400 Truth in Lending Act limit automatically. Technical precision is the only metric that matters during an audit.

Explainable AI is a non-negotiable requirement. Regulators reject "black box" decisions that cannot be interrogated. If an algorithm flags a customer interaction, your team must be able to trace the exact logic behind that assessment. This transparency ensures your compliance posture is defensible under pressure. Seamless integration with your existing stack is equally vital. Data must flow from CRMs and communication channels without manual friction to prevent corruption.

Audit-Readiness and Evidence Automation

Examiners require technical proof, not general assurances. The software must generate evidence that is fundamentally defensible through immutable audit trails. Automated Consumer Duty board reporting is a critical feature that provides a granular view of customer outcomes. You can secure your regulatory position by implementing audit-ready compliance reporting that eliminates retrospective data gathering. This ensures that every assessment is catalogued and ready for immediate inspection.

Security and Data Sovereignty

Financial institutions must prioritise platforms with proven data integrity. In high-stakes environments, cloud security is the foundation of the compliance function. Robust data encryption and strict access controls are essential to prevent unauthorised manipulation. You must ensure your provider maintains the highest standards of data sovereignty, particularly when handling sensitive customer grievances. Architectural weakness is a liability your firm cannot afford. Precision in security is as vital as precision in monitoring.

RegulaCX: The Future of Automated Audit-Ready Reporting

RegulaCX is the definitive response to the complexities of 2026 financial oversight. It is not a generic workflow tool. It is a specialised AI-Powered Compliance Intelligence Platform engineered to meet the exact requirements of the FCA and other global regulators. By deploying this complaint monitoring compliance software, organisations move beyond the limitations of human sampling. You gain the ability to scrutinise 100% of customer interactions. This ensures that no conduct risk signal remains undetected. Technical precision replaces administrative guesswork. Oversight becomes a constant state, not a periodic exercise.

Automating the Evidence Trail

The platform serves as a single pane of glass for all conduct and complaint risks. It unifies disparate data streams into a cohesive evidentiary record. RegulaCX generates audit-ready reports without manual intervention; it captures, assesses, and catalogues every interaction as it happens. Real-time risk alerting empowers your team to intervene before a systemic failure occurs. This capability is essential for maintaining the data integrity required for modern Consumer Duty Monitoring and Evidence Automation. Oversight is continuous. Evidence is permanent. Every assessment is backed by explainable logic that satisfies the most rigorous regulatory examination.

Strategic Implementation and Next Steps

The transition from fragmented data to unified compliance intelligence is a strategic mandate. RegulaCX provides the architectural foundation for this shift. It supports the Board’s annual Consumer Duty report by providing defensible, granular data that proves the delivery of good customer outcomes. You can eliminate the anxiety of regulatory scrutiny by replacing manual data unification with automated, high-velocity oversight. The path to absolute audit-readiness requires a move away from legacy systems that only record the past. It requires a system that monitors the present to protect the future.

To see how this architecture integrates with your existing technology stack, Request a technical briefing on the RegulaCX platform.

Establishing a New Standard for Conduct Oversight

The transition from administrative resolution to systemic conduct risk detection is the defining challenge for financial institutions in 2026. Legacy GRC frameworks are no longer sufficient. They lack the technical depth to unify disparate data streams and the speed to meet modern evidentiary standards. Implementing specialised complaint monitoring compliance software is the only method for achieving 100% interaction oversight whilst maintaining absolute data integrity.

By centralising intelligence and automating the evidence trail, you eliminate the manual friction that historically plagued conduct risk reporting. Precision is no longer a goal; it's a technical requirement. Your organisation can now move from a posture of vigilant protection to one of absolute regulatory certainty. RegulaCX provides the architecture necessary to bridge the gap between front-office interactions and back-office obligations.

Secure your regulatory future with the RegulaCX Compliance Intelligence Platform. Benefit from AI-powered conduct risk detection and automated Consumer Duty evidence tracking to deliver audit-ready reporting with zero manual effort. It's time to transform your compliance function into a definitive competitive advantage.

Frequently Asked Questions

What is the difference between complaint management and complaint monitoring?

Complaint management focuses on the administrative lifecycle of a ticket from intake to resolution. It is a workflow function. Complaint monitoring examines interaction data to detect systemic conduct risk across the entire customer base. By utilising complaint monitoring compliance software, firms move beyond simply closing files to identifying the root causes of dissatisfaction through 100% interaction oversight.

How does AI help in meeting FCA Consumer Duty requirements?

AI facilitates compliance by automating the collection of evidence required to prove "good outcomes" for retail customers. It continuously tracks interaction data to ensure firms meet cross-cutting rules and specific outcome mandates. This technological intervention removes the subjectivity inherent in manual sampling. It provides a defensible, data-backed record of how the firm prioritises customer interests in real-time.

Can complaint monitoring software integrate with legacy banking systems?

Modern platforms are designed to unify data from disparate legacy systems without requiring a total infrastructure overhaul. They act as a cross-system intelligence layer. This architecture bridges the gap between front-office CRMs and back-office compliance repositories. It ensures that interaction data from legacy call centres and email servers is centralised into a single source of truth for risk detection.

Does the software automate the generation of Consumer Duty board reports?

Automated software generates audit-ready board reports that require zero manual data collation. These reports provide a granular view of conduct risk and customer outcomes. This functionality allows the Board to verify compliance with Consumer Duty obligations through a single, defensible document. It significantly reduces the time spent on retrospective data gathering before annual reporting deadlines.

How does the platform identify risks for vulnerable customers?

The platform utilises sentiment analysis and machine learning to detect linguistic markers associated with customer vulnerability. It identifies signs of financial distress, cognitive impairment, or life events that require additional support. By flagging these interactions immediately, the system ensures that firms can intervene and adjust their behaviour to prevent harm. This proactive detection is a core requirement for meeting 2026 protection standards.

Is AI-driven conduct risk detection accurate enough for regulatory evidence?

AI-driven detection is highly accurate when built on sector-specific models that understand complex financial nomenclature. RegulaCX uses explainable AI to provide a transparent logic trail for every risk flag. This transparency is critical for regulatory evidence. It allows compliance officers to demonstrate exactly why an interaction was identified as a risk, ensuring the evidence is defensible during an audit.

What are the security standards for cloud-based compliance software?

Cloud-based platforms must adhere to rigorous security standards, including end-to-end encryption and strict multi-factor access controls. Data sovereignty is a priority. Systems are engineered to ensure data integrity whilst maintaining compliance with regional privacy regulations. These architectural safeguards prevent unauthorised manipulation and ensure that the evidentiary trail remains immutable for examiners.

How quickly can a firm achieve audit-readiness with automated software?

Audit-readiness is achieved continuously once the complaint monitoring compliance software is integrated into the interaction data stream. Unlike manual processes that require weeks of preparation before an examination, automated software maintains a permanent state of readiness. Every interaction is assessed and catalogued as it happens. This provides immediate access to defensible evidence whenever a regulator requests a conduct review.